Is Viking Therapeutics Stock a Bargain?

Viking Therapeutics (NASDAQ:VKTX) is a pharmaceutical startup whose stock has gone through substantial ups and downs over the last several years. While VKTX …

Viking Therapeutics (NASDAQ:VKTX) is a pharmaceutical startup whose stock has gone through substantial ups and downs over the last several years. While VKTX …

If you still associate Equifax (NYSE: EFX) with the 2017 data breach, you’re not alone. Yet the market has a short memory when a company starts …

When a founder who already controls the voting power of a company still buys millions of dollars’ worth of stock on the open market, investors should ask …

Most investors still think of automation as conveyor belts and a few orange‐painted arms. Inside Walmart’s cavernous distribution hub in Brooksville, …

The last time Berkshire Hathaway’s Class B shares traded below $500, the S&P 500 was flirting with fresh highs and short‑term Treasury bills …

The paper contract is quickly joining the fax machine in corporate museums. DocuSign (NASDAQ: DOCU) sits at the center of that transition but its share …

Alongside other high-growth tech stocks, Block (NYSE:XYZ) soared in 2021, eventually reaching an all-time high closing price of $281.81. Since then, however, …

Core Natural Resources (NYSE:CNR) is a large thermal and metallurgical coal mining company that was created in January through a merger between Arch Resources …

Electric vertical take-off and landing aircraft startup Joby Aviation (NYSE:JOBY) has seen its shares soar unexpectedly in the last week. JOBY stock is up …

Archer Aviation (NYSE:ACHR) is an aviation startup that is working to deploy electric vertical take-off and landing vehicles for uses ranging from air taxis to …

On the surface, Brown‑Forman (NYSE: BF.B) is having an unremarkable year. Class B shares change hands for roughly $29, a steep 43 % below last …

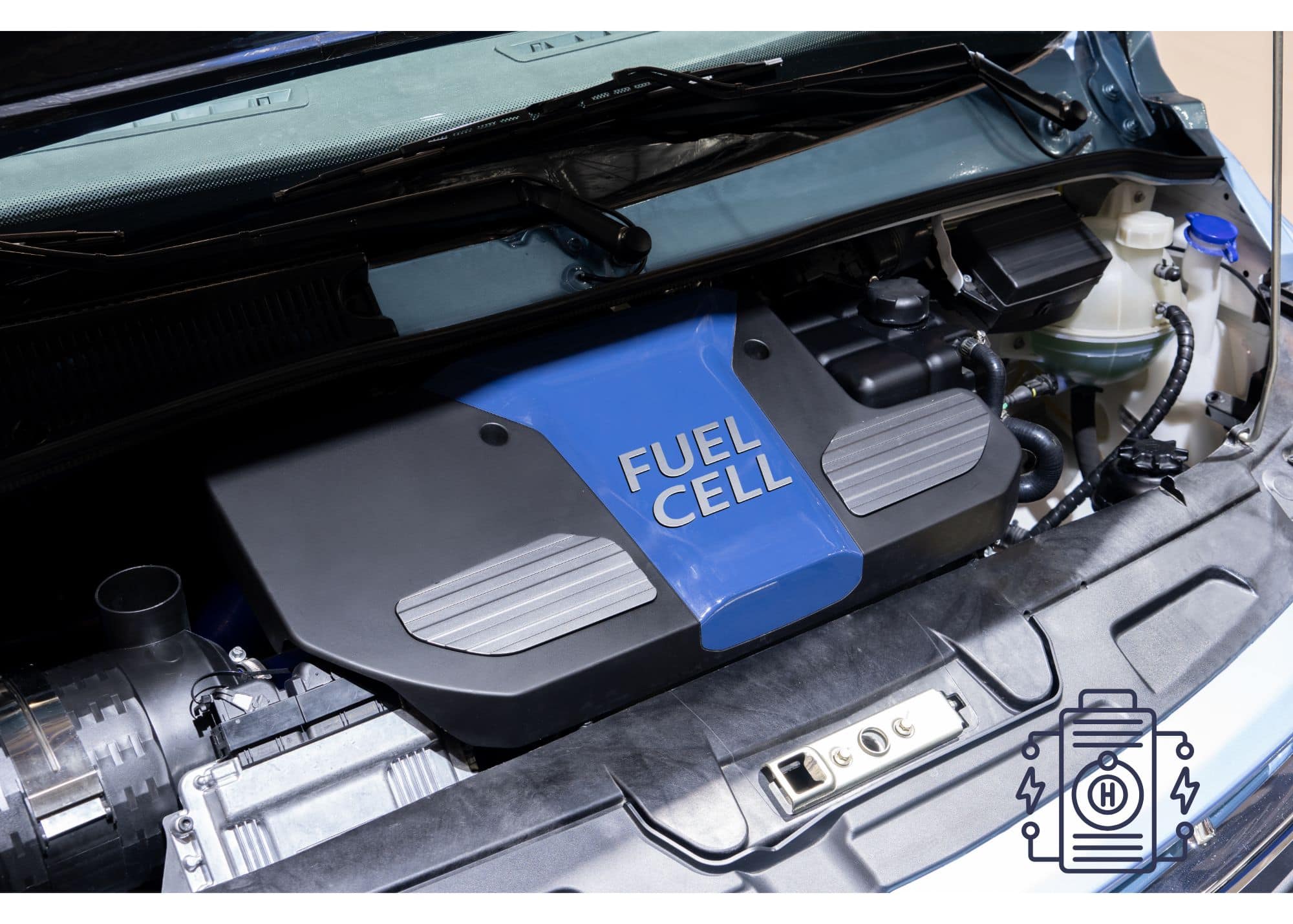

Bloom Energy (NYSE:BE) manufactures scalable fuel cells for providing on-site power. Shares in the energy startup are up over 63 percent in the last 12 months, …

GoodRX (NASDAQ:GDRX) tracks prescription drug prices and its model was so successful that it soared after its 2020 IPO, fetching $46 per share on its first day …

Freeport-McMoRan (NYSE:FCX) is among the world’s largest producers of copper and with new tariffs recently announced, FCX may be in a position to benefit …

Levi Strauss (NYSE:LEVI) is among the oldest clothing brands in the world and is almost synonymous with denim jeans. Shares of LEVI have been somewhat flat …

If you know popular consumer appliance brands Shark and Ninja, they’re both owned by SharkNinja (NYSE:SN) . With trailing 12-month returns in excess of …

Oklo (NYSE: OKLO) is only a year removed from its SPAC‑enabled debut, but its share price has already catapulted more than 193 % year to date and a …

If you stopped tracking Grab Holdings (NASDAQ: GRAB) after its 2021 SPAC listing, you probably still think of the Singapore‑based “super‑app” as a …

At roughly $89 a share, Roku (NASDAQ: ROKU) trades for barely half of the $174 intrinsic value that the most optimistic discounted‑cash‑flow model pins …

Microsoft’s market capitalization sits near $3.73 trillion today. To clear the $5 trillion bar it needs a further 35% lift about the same gain it …