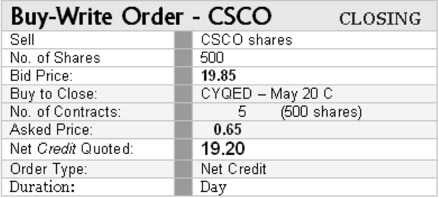

Closing a buy-write position is simply a reversal of the trade entry process: we buy back the short calls and sell the underlying stock. Let’s walk through the steps necessary to close our buy-write trade in Cisco Systems (CSCO). Here is our prospective close at current market prices:

To close the trade, we must buy back the short 20 Calls and sell the underlying stock. Since we are selling the stock and buying the calls, the trade will generate a net credit instead of a debit. Thus we will enter a limit order specifying the limit as a net credit.

If the trade is run precisely at the market quotes above, we would realize a $19.20 net credit on the trade, a profit of 0.75 on the position, before trade costs. Note that we are not required to close the trade early just because we can do so at a profit. The key is whether the closing profit is acceptable to the call writer; it’s your “call.”

It is a common-sense question of balancing the return from closing early vs. the time remaining until expiration and how much more return would be realized by remaining in the trade until expiration. If there is enough time to put on another trade in the same month, we can take this profit and put it into a new trade.

We are not in a hurry to close this position, however, since it is not threatening or moving adversely. Thus when market is 19.20, we can enter the order with a net credit of 19.25 or perhaps even 19.30. The more we get, the larger the return.

STRATEGY NOTE: If the trade was moving adversely or presenting a real danger, we would enter the closing order as a market order in order to get out quickly.

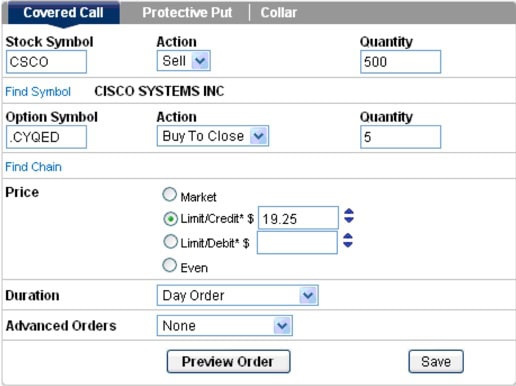

Let’s enter the closing order as a net credit limit of $19.25, in an attempt to squeeze a little more profit out of the trade. We are seeking a fatter fill on every transaction: a lower net debit on entry and higher net credit on closing. Upon closing, we must be sure to reverse the order terms used in the opening order; we must buy the short calls to close (BTC) and sell the underlying stock.

Combination Order to Open Covered Call

(Net Credit)

Assuming that we are filled at a net credit of $19.25 (instead of 19.20) we realize a net credit of $9,625.00 on the close (our opening net debit was 18.45, or $9,225.00), our return on the position would be $0.80 per share (or $80 per call contract), for a total profit of $400, before trade costs.

Figure 4.15

This represents a 4.34% return (0.80 ÷ 18.45) before commissions for a one-week trade. That’s not bad; and it’s not terribly unusual, either.

The original buy-write pulled in $1.30 of premium (we got an extra nickel from a savvy trade order), which set up a flat return of 7.0% (1.30 ÷ 18.45) for an intended trade duration of 30 days. The trader’s decision is whether to stay in the trade three more weeks to get the full $1.30 return (an extra $0.50) or to close early for the $0.80 return:

4.3% for a week vs. 7.0% for a month?

The 4.3% is the higher rate of return, but the highest rate of return is not every trader’s lodestone. More active traders will close, pocket the profit and find a new trade in the three weeks remaining until expiration. A less active trader or one with less time to find trades might let the trade go to expiration. Neither choice is “right” or “wrong.”

If unable to place the closing order as a combination order for a net credit, it will be necessary to enter separate orders to sell the stock and repurchase the calls. In this case, you must repurchase the calls first, since selling the stock first would leave the calls naked; a dangerous proposition. More to the point, your broker probably won’t allow the stock to be sold first.

If the trade was not a buy-write but instead was an overwrite of portfolio stock that we desire to keep, a closing would involve buying back the short calls only.

A Note on the Real Trade Costs

Brokerage commissions in covered call trades ranges from quite high, for the big-name brokers (who are by the way not the best for covered call trades), to $1.00 per contract, or less. I commonly hear from investors that they prefer the super-cheap discount online brokers to save costs. If the super-cheap broker is giving you 1) excellent execution, and 2) allows you to run net debit and net credit trades, then why pay more, indeed? However, the cheapest brokers don’t necessarily offer the best execution or even the “lowest” trade costs. Here’s why…

Suppose that discount Broker A charges $15 per leg (stock leg and call leg) for covered calls, which means $30 in total commission costs to place or close the position. On a five-contract trade, this works out to $0.06 per share (30.00 ÷ 5 ÷ 100), so if the premium is $0.50, you would net $0.44 after costs. Expensive? But Broker A allows the entire trade to be placed simultaneously for a net debit (credit).

Broker B has lower commissions: $5 for the stock leg, $1.00 per option contract. Thus the cost to run the five-contract trade would only be $10, or $0.02 per share (10.00 ÷ 5 ÷ 100). But – Broker B does not allow a covered call trade to be run as a combination order for a net debit or credit. Thus you have to enter the stock order, then the option order, looking to get filled on each separately. If you run both orders at market, the market will pick your pocket. And even with limit orders, prices can move unfavorably. Not to mention that you are chasing fills on two separate orders; the call leg cannot even be entered until the stock is bought.

If the poorer execution costs you $0.08 per share, it means $40 out of your pocket, plus the $10 commission: $50. How does the super-cheap commission look now? I’ve seen poor fills cost over $100 per trade. (And that’s just the opening transaction.)

Deep-discount brokers understandably are reluctant to allow online traders to talk with a live broker when needed (and for newer writers, in particular, the need could be urgent). Super-cheap means the brokerage’s employees don’t spend much, and maybe no, time yakking on the phone with customers. I recommend such firms only for experienced call writers, who rarely if ever need to deal with a human. At some deep-discount firms, it is a major exercise to talk with a customer service representative – a need everyone has, sooner or later.

Some online discount brokers offer broad and deep trading platforms with a lot of utility, but are not deep-discount brokers. Don’t expect real power and flexibility for cheap. Be aware that there is a trade-off. Don’t trade good execution for the cheapest commissions, because it is a false economy.

#1 Stock For The Next 7 Days

When Financhill publishes its #1 stock, listen up. After all, the #1 stock is the cream of the crop, even when markets crash.

Financhill just revealed its top stock for investors right now... so there's no better time to claim your slice of the pie.

See The #1 Stock Now >>The author has no position in any of the stocks mentioned. Financhill has a disclosure policy. This post may contain affiliate links or links from our sponsors.